Compare today’s mortgage refinance rates in 2026. Learn how to qualify for lower payments, save money, and refinance smartly in the USA.

7 Powerful Ways to Lock the Best Mortgage Refinance Rates in 2026

Mortgage Refinance Rates: The Ultimate 2026 Guide for American Homeowners

Imagine opening your monthly mortgage statement and realizing you could save hundreds of dollars every month simply by refinancing at a lower rate.

For many Americans, that’s not just a dream anymore. Rising living costs, credit card debt, and economic uncertainty have pushed homeowners to search for smarter ways to manage money. One of the biggest financial opportunities in 2026 is taking advantage of lower mortgage refinance rates before the market shifts again.

But here’s the truth most people don’t realize: refinancing is not only about getting a lower interest rate. Done correctly, it can help you reduce monthly payments, pay off debt faster, shorten your loan term, or even tap into home equity for important expenses.

The challenge? Mortgage lenders flood the internet with confusing offers, hidden fees, and flashy advertisements that make everything sound “too good to be true.”

This guide breaks everything down in plain English so you can confidently understand today’s mortgage refinance rates, compare lenders wisely, and decide whether refinancing makes financial sense for your situation in 2026.

What Are Mortgage Refinance Rates?

Mortgage refinance rates are the interest rates lenders offer when you replace your current home loan with a new one.

Homeowners refinance for several reasons:

- Lower monthly payments

- Better interest rates

- Switching from adjustable to fixed rates

- Paying off the loan faster

- Accessing home equity cash

- Removing mortgage insurance

Your refinance rate depends on factors like:

| Factor | Impact on Rate |

|---|---|

| Credit Score | Higher score = lower rates |

| Loan Term | Shorter terms often have lower rates |

| Home Equity | More equity improves approval chances |

| Debt-to-Income Ratio | Lower debt helps secure better offers |

| Loan Type | FHA, VA, conventional, and jumbo loans vary |

In 2026, many homeowners are closely watching mortgage refinance rates because even a 1% difference can save tens of thousands of dollars over the life of a loan.

Why Mortgage Refinance Rates Matter More in 2026

The housing market has changed dramatically over the past few years.

Interest rates surged after inflation concerns, and millions of Americans became trapped in higher mortgage payments. Now, with signs of market stabilization, refinance opportunities are returning.

That means homeowners who missed low rates previously may finally have another chance to save money.

Refinancing Can Potentially Help You:

- Save $200–$800 monthly

- Reduce total loan interest

- Consolidate high-interest debt

- Build equity faster

- Improve long-term financial stability

For families struggling with rising costs, competitive mortgage refinance rates can provide meaningful financial relief.

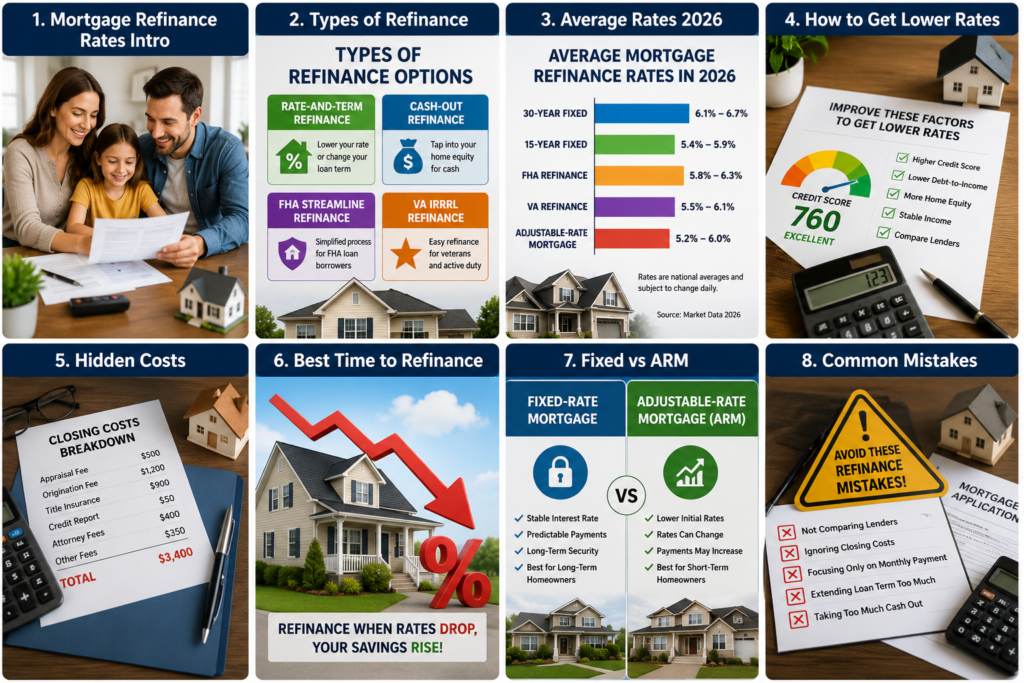

Current Types of Mortgage Refinance Options

Understanding refinance types helps you choose the right strategy.

Rate-and-Term Refinance

This is the most common refinance option.

You replace your current mortgage with a new loan that has:

- A lower rate

- Different loan length

- Better terms

Best for:

- Lower monthly payments

- Paying less interest over time

Cash-Out Refinance

A cash-out refinance allows homeowners to borrow against home equity.

Example:

If your home is worth $500,000 and you owe $300,000, you may refinance and take part of the remaining equity as cash.

People use this for:

- Home renovations

- Debt consolidation

- Medical bills

- College expenses

However, cash-out loans usually have slightly higher mortgage refinance rates.

FHA Streamline Refinance

Designed for homeowners with FHA loans.

Benefits include:

- Reduced paperwork

- Faster approvals

- Lower closing costs

VA IRRRL Refinance

Available for veterans and active military members.

Advantages:

- Minimal documentation

- No appraisal in many cases

- Competitive rates

Average Mortgage Refinance Rates in 2026

While rates change daily, national averages generally look like this:

| Loan Type | Average Rate |

|---|---|

| 30-Year Fixed Refinance | 6.1% – 6.7% |

| 15-Year Fixed Refinance | 5.4% – 5.9% |

| FHA Refinance | 5.8% – 6.3% |

| VA Refinance | 5.5% – 6.1% |

| Adjustable-Rate Mortgage | 5.2% – 6.0% |

Remember:

Your personal rate may differ based on financial qualifications.

That’s why comparing multiple lenders is critical when shopping for mortgage refinance rates.

How to Get the Lowest Mortgage Refinance Rates

Many homeowners unknowingly accept higher rates than necessary.

Here’s how smart borrowers secure better deals.

Improve Your Credit Score

Credit scores significantly impact refinance offers.

Tips to boost scores:

- Pay bills on time

- Reduce credit utilization

- Avoid new debt before refinancing

- Check credit reports for errors

Generally:

- 740+ credit scores receive the best rates

- 620–680 scores may pay higher interest

Increase Home Equity

Lenders prefer borrowers with substantial equity.

The more equity you have:

- The safer you appear to lenders

- The lower your risk profile

- The better your refinance terms

Aim for at least 20% equity whenever possible.

Compare Multiple Lenders

Never accept the first offer.

Request quotes from:

- Banks

- Online lenders

- Credit unions

- Mortgage brokers

Even small differences in mortgage refinance rates can create major long-term savings.

Choose a Shorter Loan Term

15-year refinance loans often have lower rates than 30-year loans.

Benefits:

- Faster payoff

- Lower total interest

- Faster equity growth

Tradeoff:

Monthly payments may be higher.

Hidden Costs Most Homeowners Ignore

Refinancing is not free.

Closing costs usually range from 2% to 5% of the loan amount.

Common Refinance Fees

| Fee Type | Estimated Cost |

|---|---|

| Appraisal | $300–$700 |

| Origination Fee | 0.5%–1% |

| Title Insurance | $500–$1,500 |

| Credit Report | $25–$50 |

| Attorney Fees | Varies |

Always calculate your “break-even point.”

Example:

If refinancing costs $4,000 and saves you $200 monthly, your break-even point is 20 months.

If you plan to move before then, refinancing may not make sense.

Best Time to Refinance Your Mortgage

Timing matters.

You should consider refinancing when:

- Rates drop at least 1%

- Your credit improves significantly

- You want a fixed-rate mortgage

- Your home value increases

- You need lower monthly payments

Many financial experts believe homeowners should monitor mortgage refinance rates regularly rather than waiting for headlines.

Small market shifts can create huge savings opportunities.

Fixed vs Adjustable Refinance Rates

Fixed-Rate Mortgage Refinance

Your interest rate stays the same.

Best for:

- Stability

- Long-term homeowners

- Predictable payments

Adjustable-Rate Mortgage (ARM)

Rates change periodically after an initial fixed period.

Best for:

- Short-term homeowners

- People expecting future income growth

Risk:

Monthly payments may increase later.

Most American homeowners still prefer fixed mortgage refinance rates for financial security.

Common Refinance Mistakes to Avoid

Refinancing can be powerful, but mistakes can become expensive.

Focusing Only on Monthly Payments

Lower payments may extend your loan term and increase total interest paid.

Always review:

- Total loan cost

- Interest paid over time

- Loan duration

Ignoring Closing Costs

Some lenders advertise “no closing costs,” but fees are often rolled into the loan balance or higher rates.

Read every document carefully.

Applying With Poor Credit

A few months of credit improvement can dramatically reduce mortgage refinance rates.

Patience often pays off.

Taking Too Much Cash Out

Using home equity irresponsibly can create future financial problems.

Borrow only what you truly need.

How the Federal Reserve Impacts Mortgage Refinance Rates

Mortgage rates are heavily influenced by:

- Inflation

- Treasury yields

- Federal Reserve policies

- Economic growth

When inflation cools:

- Mortgage rates often decline

When inflation rises:

- Rates typically increase

While the Federal Reserve does not directly set mortgage rates, its decisions strongly affect lender pricing.

This is why news about interest rates often impacts refinance activity across the United States.

Should You Refinance in 2026?

The answer depends on your goals.

Refinancing May Be Worth It If:

- You can lower your rate significantly

- You plan to stay in your home long-term

- You want predictable monthly payments

- You need to consolidate debt

- You want to pay off your mortgage faster

Refinancing May Not Be Ideal If:

- You plan to move soon

- Closing costs outweigh savings

- Your credit score is weak

- Your financial situation is unstable

Carefully comparing mortgage refinance rates and calculating long-term savings is essential before making any decision.

Expert Tips for First-Time Refinancers

If this is your first refinance, follow these smart strategies.

Keep Documents Ready

Lenders usually request:

- Tax returns

- Pay stubs

- Bank statements

- W-2 forms

- Mortgage statements

Lock Your Rate Quickly

Mortgage rates can change daily.

If you find a strong offer, consider locking it before market conditions shift.

Avoid Major Financial Changes

During the refinance process:

- Don’t open new credit cards

- Don’t finance a vehicle

- Avoid large bank withdrawals

Lenders monitor financial activity closely before approval.

Conclusion

For millions of Americans, refinancing in 2026 could become one of the smartest financial decisions of the year.

The key is understanding how mortgage refinance rates work, comparing lenders carefully, and focusing on long-term savings instead of flashy marketing promises.

A lower rate can reduce stress, improve monthly cash flow, and create greater financial stability for your family. But refinancing only works when it aligns with your goals and future plans.

Take time to review your finances, improve your credit profile, and shop around before signing anything.

The right refinance strategy today could save you tens of thousands of dollars tomorrow.

Frequently Asked Questions

What credit score is needed for mortgage refinancing?

Most lenders prefer a credit score of at least 620, but the best mortgage refinance rates usually go to borrowers with scores above 740.

How long does refinancing take?

Most refinance processes take 30–45 days depending on the lender and loan complexity.

Can refinancing hurt my credit score?

Refinancing may temporarily lower your score slightly due to hard inquiries, but long-term financial improvement can outweigh the impact.

Is refinancing worth it for a 1% lower rate?

In many cases, yes. Even a 1% reduction can save thousands over the life of the mortgage.

Can I refinance with bad credit?

Yes, but you may receive higher interest rates and stricter loan terms.